European Manifesto – Why the cultural & creative sectors must unite

WHY THE CULTURAL & CREATIVE SECTORS MUST UNITE – AND WHY THEY SHOULD BE TREATED AS A KEY SECTOR: BARRIERS TO INNOVATION, AND SOLUTIONS FOR A STRONG INNOVATIVE ENVIRONMENT FOR CULTURE AND CREATIVITY IN EUROPE

- Where do we see a problem?

In the growing innovation gap between technology and culture: Digitisation and new technologies such as artificial intelligence, virtual and augmented reality, blockchain, 3-D printing and big data can trigger innovation at all levels of the creative sectors. However, although there are plenty of innovative initiatives and start-ups in the creative and cultural sectors, very few of these reach a scale sufficient for them to have a bigger impact on society or the market.[1] We can see a growing gap between technology and culture. Culture, and with it society, are struggling to catch up with the exponential speed of technological innovation.

Figure 1: The technology/culture innovation gap; © THE ARTS+/ Frankfurter Buchmesse GmbH

This innovation gap is not only relevant for the creative sectors, it is relevant for us all – citizens, societies and culture at large. Digitisation and new technologies can have a big impact on the diversity of cultural activities and content. Depending on the framework we as a society set, this impact can be negative or positive. For culture and the creative sectors, therefore, the need to address common challenges and identify opportunities in the face of digital technologies underpins their very survival. Not only do we need these sectors to survive, we need them to thrive in the digital age. Culture is one of Europe’s biggest assets. But in an era of big technological change, Europe needs a more effective innovation strategy for culture. Right now, the logic of the big commercial platforms is reshaping not only Europe’s markets, but also its societies. Culture helps us make sense of our world, and it should provide a moral compass for technology. We must ensure that technology serves human beings, not the other way round. To empower culture in that function as moral compass, and to empower citizens to make the most of culture, massive public support is needed for innovation in culture, but such support is currently lacking. Here are some examples of what is happening while we, as citizens, are failing to appreciate the urgency of the need to support innovation for culture:

- The shift from the “Gutenberg Galaxy” (which, for more than 550 years, revolved around reading and writing as the preeminent cultural techniques for the structuring of knowledge and communication) to the digital age is being shaped by the markets alone, rather than being the focus of a wider discussion within society and of a shared cultural understanding. Pushed by the need to compete with big platforms, there is a growing trend toward market concentration in book publishing. This translates into less diversity and a less healthy market. If we want to maintain the function of books as vital and diverse sources of entertainment and knowledge for our societies and democracies, and to integrate reading and writing as meaningful cultural techniques within the digital ecosystem, we need to act now.

- Journalism is of fundamental importance for a properly functioning democracy, and for social cohesion, education and cultural development. But in terms of content distribution and advertising revenues, the media organisations increasingly have to compete with large digital players in the information business. Journalism has seen a steady decline in revenues since the onset of the digital age, with 85% of the main digital source of income – advertising – now being claimed by Facebook and Google alone, globally. [2] Click-driven business models make a lucrative business out of phenomena such as “fake news”. This results in consciously driven misinformation on a large scale. “Click-bait” and politically motivated misinformation campaigns are (still) held in check by the influence of high quality journalism. As some journalism outlets are turning to corporate subscription models in response to this crisis in business models, there is a risk that being well-informed will become the privilege of the few who are willing and able to pay for journalism, and not the many. We need to sustain a diverse, high-quality and independent press, through sustainable business models and constant innovation, thereby providing an alternative to social media and search engines as our main sources of information.

- If museums are to stay relevant in the future, they need to maintain a strong presence that lets them connect to different sections of society at all levels and through all channels. This requires the technological and digital development of those organisations, as rapidly as possible. For instance, capacity building is a priority for the heritage and cultural sectors – indeed it is a prerequisite if we are to overcome the prevailing approach that views digital technologies only as tools for accessing, using and disseminating cultural heritage, rather than as the means of creating new content. If museums lose their relevance, we will also lose their valuable function as places that foster dialogue in a democratic society and stimulate creativity and learning.

At present, it seems that each player is grappling alone to overcome this innovation gap. But what if there was a wider European ecosystem of support for innovation, one that cut transaction costs and boosted the creative sectors to a digital level? What if the united creative sectors had all the opportunities that befit their combined rank as a European key sector – a sector whose significance in terms of jobs compares to the likes of the automotive and chemical industries, and which is far more important in its cultural and societal impact?

But what are the best ways to support tech-driven innovation in the cultural and creative sectors? These sectors are very good at communicating other people’s messages and stories, but when it comes to articulating their own interests their voice is surprisingly weak. This has a lot to do with fragmentation, as the majority of creative players are micro-entities. On top of that, the creative sectors are not (yet) united, but often still work in “sectoral silos.” [3]

In the past decade several studies highlighted the social, economic and cultural relevance of the creative sectors. Taken together, the 11 sub-sectors of the creative industries provide “more than 12 million full-time jobs, which amounts to 7.5% of the EU’s workforce, creating approximately EUR 509 billion in value added to gross domestic product (5.3% of the EU’s total gross value added).”[4] In 2016, the European Parliament demanded – finally! – a coherent policy for the creative sectors as a European key sector: “What we need is a comprehensive industrial strategy at the European level that will take all specific characteristics of cultural and creative industries into account, and will turn challenges like digitalisation (…) into new growth and job opportunities.”[5] This report, written jointly by the industry and culture committees of the European Parliament, is a rare and splendid example of what can happen if industry and culture put their heads together. But to create a coherent policy, first and foremost we need a strong and united voice for the cultural and creative sectors. This is currently still lacking[6] – despite calls from people such as Christian Ehler, of the European Parliament’s industry committee, who warns that each of the sectors alone is far too weak, and that they need to unite to find a strong voice.

We support the demands of the European Parliament’s report and urge the swift implementation of a coherent innovation policy for the creative sectors at European, national and regional levels. We concur with other players like Culture Action Europe, who demand a one per cent increase in European culture budgets.[7] In our Manifesto, we highlight the six main structural problems for innovation in the cultural and creative sectors (problems which have been identified in numerous studies – see below, p. 11 ff), and we recommend solutions that would support innovation for culture at European and national levels. We want to increase the awareness of citizens, policy makers and society at large of the problems the cultural sectors currently face when it comes to technologically driven innovation – and what it will take to boost culture into the digital age. This Manifesto is an important step toward finding a strong and united voice for our combined sectors. We have begun the process from the perspective of journalism and broadcasting, book publishing and cultural heritage – and we have already identified challenges we face in common. Now we would encourage other cultural and creative sectors to join us in our initiative.

II. The six main structural problems for innovation in the cultural and creative sectors

at the European, national and regional levels

- High fragmentation

- The cultural and creative sectors are characterised by high levels of micro-entrepreneurship and self-employment. companies with fewer than 10 employees account for more than 95% of the sectors’ players.[8] At the same time, the digital economy encourages platformisation and monopolisation on the part of the intermediaries, i.e. big tech companies (Google, Amazon, Facebook, Apple). The discrepancy between fragmentation and platformisation results in an uneven playing field and creates problems such as the “value gap” (the disparity between the high demand for creative content online, and the low remuneration). Other problems include poor interoperability and use of standards;[9] a lack of viable business models; shortfalls in political representation; the increasing digital divide; etc.

- Strong silos: The cultural and creative sectors work largely in isolation from each another, as well as from other sectors. At the same time, political structures (sector ministries, etc.) also exhibit a lack of joined-up thinking. This hinders unity in the actions of the different players and sectors. The very term “cultural and creative sectors” indicates a top-down approach, since it is mostly used by political or administrative players, while the reality on the ground does not yet reflect such integration. Digitisation and new technologies have only just started paving the way for broader convergence, while the political structures do not yet reflect the growing need for unity.

- Fragmentation and the tendency to work in silos also reinforce the conservative culture and mind-set of some players in the creative sectors. There is little will or experience for “thinking big” in the cultural and creative sectors as a whole (due to their fragmented character), and the knowledge and experience needed for cooperation and innovative activities at the institutional level are also lacking.

- Lack of investment, funding and financing

- The cultural and creative sectors are notoriously underfinanced and their huge potential remains largely untapped. This is the result of a perceived lack of financial credibility, attractiveness and scalability. The individual sectors are obliged to invest in innovation for themselves, with hardly any outside investment forthcoming (unlike in sectors such as biotech, robotics and ICT).

- There are also very few dedicated public funding policies in place of a noteworthy scale. Already in 2011, it was estimated that a financing gap of between EUR 2.8 billion and EUR 4.8 billion existed, in terms of bank loans for cultural and creative SMEs.[10] Publicly funded institutions are often also underfinanced, as national cultural budgets are in decline across Europe.

- Specific characteristics of the cultural and creative sectors

Many aspects of innovation specific to these sectors are not (yet) acknowledged, are not (yet) measurable in all their different dimensions and as such do not (yet) find recognition in public policies.

- There is a focus on intangible assets – e.g. intellectual property (IP), e-content as a service, people-centred assets, such as creativity, experience and social and cultural impact. Intangible assets are not easily measured or understood, although there is a great need to do so, since all digital assets are essentially intangible.

- “Soft innovation” is a prevalent concept in the creative sectors – e.g. cultural, social and content innovations, new processes and business model innovation. This is something that players outside these sectors find harder to understand than “hard” technological innovation.

- These sectors are knowledge- and labour-intensive. This implies that they often rely more on established practices than on technologically driven innovation. This can present barriers to innovation as it makes traditional approaches to scaling up quite difficult. Yet on the other hand it offers huge employment opportunities within the digital environment.

- Most creative sectors are subject to extensive regulation of a specific kind. Due to the public interest in creative content and the works produced by the cultural and creative sectors, states often exert a greater influence on them than on other sectors – for instance, through regulation. It can be hard to strike a balance between the need to ensure wide access to culture, on the one hand, and the creators’ need for incentives to produce cultural works, on the other. The US platforms operate across different sectors and away from national and sector-specific regulatory frameworks. These, on the other hand, do still regulate the European players.

- Some sectors (audio-visual production, the fine arts, cultural heritage, etc.) exist with high levels of public funding and/or public governance. Despite this, there are hardly any innovation support structures specific to the cultural and creative sectors at regional, national or European levels.

- Lack of integration of technical and entrepreneurial skills; potential loss of “traditional” values and know-how

- While the cultural and creative sectors often draw on strong behavioural, social, creative and critical thinking skills, there is a marked lack of integration of technical and entrepreneurial skills. There are various reasons for this.[11] One factor is the lack of appropriate education and training, another is the low influx of IT-savvy professionals from other sectors, due to the comparatively low pay and image problems of the creative sectors.

- Conversely, there is also a danger that existing values and capacities will be lost with the digital shift. As one example, digitization threatens to undermine the distinction between editorial and marketing roles, which was always an important pillar of the “old” media.

- Value chains are changing, bringing a need for new value/business models

- In the cultural and creative sectors most business models still rely on paid content (or, in digital terms, paid services) and advertising. This is now being challenged by big, often monopolised platforms which generate their income from hardware and software sales, and – overwhelmingly – from The advertising income also derives from the unprecedented sale of costumers’ data. This business model is only possible for the big players – who are, moreover, often unwilling to share that customer data with the cultural and creative sectors. None of the big platforms has a genuine business interest in paid content: content is often a free add-on for their channels in order to generate more traffic, and thus more advertising/data. This encourages a “for free” culture on the internet, and makes the paid content business model even more difficult to sustain.

- Scaling up activities is different for creative companies than for companies in other sectors (see point 3).

- Internationalisation remains a challenge, not least because of regulatory issues, but also because of the challenge of transforming a territorial and language-based business model into a digital, globally oriented business model – compounded by the lack of a single digital market.

- Value models in publicly funded institutions are under pressure due to the reduction in funding levels.[12] Such institutions now face the challenge of finding new revenue sources. Before the 2008 financial crisis, average public spending on cultural services in Europe was growing by five per cent a year; since then, it has fallen by one per cent each year.[13] Cultural spending by governments accounts for only one per cent of the GDP of the EU28 – a share that has remained unchanged for more than a decade, behind defence (1.4%) and education (4.9%).[14] The distinction between “publicly funded” and “commercially funded” is not useful for the creative players, as there is an increasing hybridisation of private, public and third-sector structures, although mainstream structures still preserve this artificial – and politically motivated – duality.

- Culture and creativity exist in an increasingly global context and require an international approach

- This is true not only from an economic point of view (e.g. exports and internationalisation: a considerable amount of revenue comes from international business), but also from a creative point of view (creative works are often the product of international cooperation). It also applies to the reception of creative works, which ideally is often international. However, public institutions and creative players often think and act with a silo mentality, focusing only on specific sectors. Moreover, the cultural and creative sectors have to respond to national regulations and legislation, which prevents them from operating fully and successfully at the international level.

III. How can we overcome these structural barriers?

The six most relevant innovation support measures for the cultural and creative sectors at the European, national and regional levels:

- Acknowledge the converging and “hybrid” structures of the cultural and creative sectors, which operate at the intersection between culture, business, technology and politics:

- Support their innovation potential for the wider economy through more explicit policies.

- Encourage “out of silo” activities and policies.

- Explicitly target commercial and non-commercial cultural and creative players.

- Form coherent policies at EU and national levels to encourage a cross-sectorial ecosystem for the cultural and creative sectors.

- Support the gathering of knowledge about specific innovation needs through collaborative European research, through ecosystem building and through cooperation with creators, companies, creative entrepreneurs and industry stakeholders (“innovation knowledge” is often locked inside the sectors and not yet readily available to scientific research).

- Establish a research body with EU-wide coverage (e.g. taking the European Audiovisual Observatory or the Copyright Hub or the European Digital Reading Laboratory as examples).[15]

- Raise public investment in the cultural and creative sectors to a level which befits their relevance as a key sector, and tailor funding programmes to their needs:

- The public sector should dedicate a significant proportion of the innovation budgets at national, regional and EU levels to culture and creativity. This should include strengthening sector-specific actions (e.g. Creative Europe) as well as integrating innovation support for the cultural and creative sectors into crosscutting programmes. We call for culture and the creative sectors to be seen and treated as a key component of innovation in the industry funding policies that target the digital transformation in general.[16] Such policies include the EU’s planned funding programmes Horizon Europe, Digital Europe[17] (especially the Digital Innovation Hubs and the European Innovation Council), the single market programme COSME,[18] the InvestmentEU Programme[19] and the European Structural and Investment Funds. At present, the only EU support programme that addresses culture is Creative Europe. The EU is planning to provide EUR 1.85 billion for this programme over the seven-year period 2021-2027. This amounts to around EUR 264 million per year[20] and represents just appr. 0.15% of the total EU budget.[21] By comparison, the EU’s planned overall investment in defence – the European Defence Fund – for the post-2020 funding period is EUR 13 billion, or EUR 1.86 billion per year.[22]

- The cultural and creative sectors require funding that is not only project-driven, but which also supports long-term objectives. This should allow for experimentation and risk-taking, while keeping levels of bureaucracy to a minimum. It is also important to fund “intangible infrastructure”, ensuring interoperability and the transferability of content between platforms; promoting the development of standards and the creation of data (and big-data) infrastructure – also for data management in the field of IP rights; and introducing technologies to help the creative sectors fulfil social goals, such as accessibility.

- Make it easier and more attractive to invest in innovation for the cultural and creative sectors:

- Strengthen alternative forms of investment, such as crowdfunding, donations, patronage, and revenues – where micro-payments are key to the development of forms of pay-per-content at different level of granularity

- Make cultural and creative sectors an integral part of general industry initiatives, such as the InvestEU Programme.[23]

- Implement incentives such as tax breaks for creative and cultural entrepreneurs or financiers, e.g. when investing in digital infrastructure or other innovation support measures.

- Strengthen European initiatives like the Cultural and Creative Sector Guarantee Facility[24] (which aims to ease banking institutions’ credit conditions for the creative sectors) and extend these initiatives to other forms of public and private investment.

- Strengthen the dialogue between policy, culture, technology and business/industry stakeholders, as well as intermediaries, research actors and civil society, with respect to innovation in the cultural and creative sectors:

- Establish new forms of engagement through physical events and forums

- Provide incentives for the involvement of cultural and creative actors (entrepreneurs, companies, creators) and for capacity building measures for intermediaries (associations, networks, cluster organisations, hubs, festivals etc.), especially those that promote cooperation within each sector and with other related sectors.

- There is a real need for the public sector to forge a partnership with the cultural and creative sectors, not only when it comes to policy making, but also in terms of public procurement.

- Promote a broader definition of innovation that goes beyond just “hard” technological innovation:

- Include “soft” innovation (content-related, cultural, social, process and business model innovation, etc.).

- Support research, development and innovation (R&D&I)-driven approaches within the cultural and creative sectors, while also encouraging the adaptation of existing technologies and market-uptake, as well as interoperability and standardisation.

- Support cooperation between research institutions and cultural and creative actors.

- Foster interdisciplinary partnerships.

- Open innovative, digital and creative hubs.

- Develop an adequate measuring framework for multi-dimensional values created.

- Include training as an integral part of innovation, in both educational (schools, universities) and professional contexts.[25]

- Increase the international character of the cultural and creative sectors:

- Strengthen supranational policies and innovation support measures, especially at EU level

- Increase the focus on international issues within national and regional institutions

- Encourage cross-sectorial encounters and cooperation.

- Strengthen the cultural and creative sectors as an integral part of the European digital single market.

IV. Approach

We have now identified the six most relevant structural obstacles to innovation, and formulated the six most relevant innovation support needs for the cultural and creative sectors, at regional and national and European levels.

The European Manifesto on Supporting Innovation for Culture & Creative Sectors is an outcome of THE ARTS+ Innovation Summit (10 October 2018), which was organised as part of ALDUS (the network of European Book Fairs, www.aldusnet.eu(Öffnet neues Fenster)) and is co-funded by the Creative Europe Programme of the European Union.

The Manifesto is the result of cooperation between 14 partners in THE ARTS+ Innovation Summit(Öffnet neues Fenster) – among whom, THE ARTS+ and its strategic partners, the European Creative Business Network (ECBN)/european centre for creative economy (ecce) and the Fitzcarraldo Foundation/ArtLab have taken the lead, working together for several months in the run up to the Summit.

The descriptions of the structural obstacles and support needs are drawn from a number of existing studies and recommendations regarding the cultural and creative sectors in general, at the European level (see p.12 below). The network of partners mainly worked to prioritise the obstacles and the support needs, and to find consensus with respect to their validity in such different sectors as book publishing, journalism, broadcasting and cultural heritage – and in the cultural and creative sectors more generally.

The Manifesto, presented at a press conference on 11 October 2018(Öffnet neues Fenster), is also available online (https://theartsplus.com/category/blog/(Öffnet neues Fenster)) and through the partners’ various communication channels. The insights collected here should form the basis for a further discussion with experts from the fields of culture, business, technology and politics.

Strategic Partners

- Fitzcarraldo Foundation http://www.fitzcarraldo.it/en(Öffnet neues Fenster) /ArtLab fitzcarraldo.it/en(Öffnet neues Fenster) (Italy)

- European Creative Business Network (ECBN) (Netherlands)/ european centre for creative economy (Germany) (ecce), http://ecbnetwork.eu/who-we-are/(Öffnet neues Fenster); https://www.e-c-c-e.de(Öffnet neues Fenster)

Programme Partners

- ALDUS – European Book Fairs’ Network, aldusnet.eu(Öffnet neues Fenster)

- Europeana Foundation, http://www.europeana.eu(Öffnet neues Fenster) (Netherlands)

- Federation of European Publishers (FEP) http://fep-fee.eu(Öffnet neues Fenster)/ (Belgium)

- German Publishers and Booksellers Federation Boersenverein.de(Öffnet neues Fenster) (Germany)

- Italian Publishers Association (AIE) aie.it (Italy)

- Studies in Media, Innovation and Technology (SMIT), research group at the Vrije Universiteit Brussel (VUB) & part of imec, Flanders/ partner of the EU-funded project MediaRoad http://smit.vub.ac.be/(Öffnet neues Fenster) https://www.imec-int.com(Öffnet neues Fenster); http://www.mediaroad.eu/(Öffnet neues Fenster) (Belgium)

- The Network of European Museum Organisations (NEMO) ne-mo.org/(Öffnet neues Fenster)

Network Partners

- Deutscher Museumsbund e.V., museumsbund.de(Öffnet neues Fenster) (Germany)

- Fundación Germán Sánchez Ruipérez, http://fundaciongsr.org(Öffnet neues Fenster)/ (Spain)

- German Commission for UNESCO www.unesco.de(Öffnet neues Fenster) (Germany)

- I3, a coordinated support action (CSA), funded by the European Commission under the European research funding programme Horizon2020, represented by T6 Ecosystems; eu/(Öffnet neues Fenster), http://www.t-6.it/(Öffnet neues Fenster) (Italy)

- New European Media (NEM)/ VitalMedia, http://nem-initiative.org(Öffnet neues Fenster)

- World Association of Newspapers and News Publishers (WAN-IFRA)/ Global Alliance for Media Innovation, http://www.wan-ifra.org(Öffnet neues Fenster), http://media-innovation.news/(Öffnet neues Fenster) (France)

Editorial group of the Manifesto

and members of the 14 partners of THE ARTS+ Innovation Summit 2018

Chaired by

Nina Klein, THE ARTS+; Ugo Bacchella, Fitzcarraldo Foundation/ArtLab; Bernd Fesel, European Creative Business Network (ECBN)/european centre for creative economy (ecce)

Editorial group

Julia Pagel, NEMO; Harry Verwayen, Europeana Foundation; Enrico Turrin, Federation of European Publishers (FEP); Piero Attanasio, Italian Publishers Association (AIE); Cigdem Aker, German Publishers and Booksellers Association; Octavio Kulesz, Editorial Teseo/UNESCO; Christine M. Merkel, German Commission for UNESCO; Andrea Wagemans, WAN-IFRA/GAMI; Heritiana Ranaivoson, SMIT/imec/Mediaroad; Luis González, Fundación Germán Sánchez Ruipérez; Simona de Rosa & Andrea Nicolai, T6 Ecosystems/ I3; Pierre-Yves Danet, Orange Labs/New European Media/ VitalMedia, David Vuillaume, Deutscher Museumsbund

Editing & proofreading: Alastair Penny

The consensus building took place in a number of physical meetings and workshops, and in several virtual meetings. Two workshops were organised, one focusing on book publishing & innovation support (in Frankfurt am Main, 18 February 2018, in cooperation with the German Publishers and Booksellers Association), the other focusing on Cultural Heritage and innovation support (in Milan, 24 May 2018, at ArtLab Milan(Öffnet neues Fenster), in cooperation with the Fitzcarraldo Foundation/ ArtLab, with support from the Network of European Museum Organisations, NEMO, and the European Creative Business Network (ECBN)/ european centre for creative economy (ecce)). The findings were validated with a group of 100 experts as part of THE ARTS+ Innovation Summit(Öffnet neues Fenster) (10 Oct 2018).

- Basic definitions:

What are we talking about when we say …

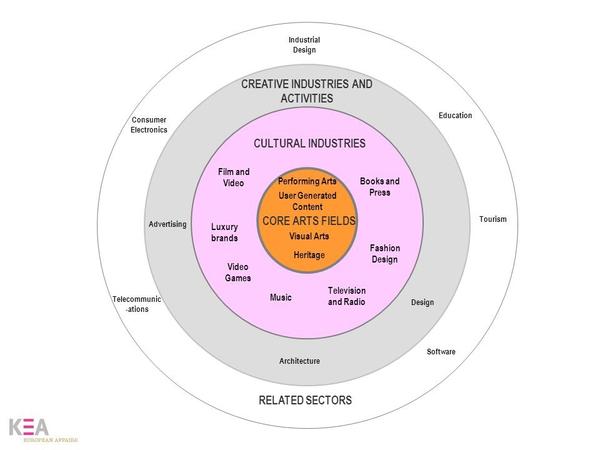

… cultural and creative sectors:

Figure 2: what are the creative and cultural sectors? © European Affairs KEA[26]

… technologically driven innovation: Digitisation and new technologies such as AI, VR/AR, 3-D printing, Internet of Things (IoT) and others, trigger innovation at all levels of the cultural and creative sectors. This might relate to their social or cultural impact, to the content, products and services, to processes and marketing/outreach, to organisational cultures, business models and value networks, or to skills and competences, and more besides. Innovation is understood as anything which is new and adds value, be it economic, social or cultural value.

…innovation support: Support for:

– technological innovation/ research, development and innovation (R&D&I)

– adaptation and adoption of technological innovation

– content (new formats, new storytelling, etc.)

– services & products (user experience, design, unique value proposition, content ….), marketing

– organisational culture (processes, innovation climate, organisational models …)

– business and value models (new funding frameworks, new revenue streams, new channels, new markets, new value networks, new partnerships, new target groups…)

– development of skills & competences (social/creative/critical/technical/ entrepreneurial …)

– and other levels …

… targets and instruments of innovation support: public image & awareness, infrastructure, capacity building (networks, cooperations, know-how, skills & competences, internationalization…), financial support. A few examples: tax incentives, public funding & public finance for innovation, labour market intervention, standard-setting, communication & awareness raising

- Sources: Literature on the creative and cultural sectors and tech-driven innovation

Culture Action Europe: Position on post Multi-Annual-Framework of the EU Budget,

https://cultureactioneurope.org/advocacy/cae-position-on-post-2020-mff/(Öffnet neues Fenster)

CAE Manifesto: 1% for Culture. Supporting culture is supporting Europe,

Cultural Heritage 3.0: Audience and access in the digital era, Conference, Estonian National Museum, 2017, Livestream, URL: https://livestream.com/eu2017ee/events/7593350(Öffnet neues Fenster)

European Creative Business Network (ECBN): The Cultural and Creative Industries in Europe. Entrepreneurial assets and capacities need more support. Ed. by Johanna von Antwerpen, Bernd Fesel, Laure Kaltenbach, 2015, http://ecbnetwork.eu/wp-content/uploads/2015/07/ECBN_Manifesto-20151.pdf(Öffnet neues Fenster)

European Parliament: Report on a coherent EU policy for the cultural and creative industries, 2016, URL: http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT+REPORT+A8-2016-0357+0+DOC+XML+V0//EN(Öffnet neues Fenster)

Europeana: Uncharted Territory. discussing ‘digital’ strategy for cultural heritage institutions at the Frankfurt Book Fair, 2017, URL

European Policy Brief: The Cultural Heritage Institution: Transformation and Change in Digital Age. RICHES Project, 2016, URL: http://www.digitalmeetsculture.net/wp-content/uploads/2016/04/EUROPEAN-POLICY-BRIEF_Institutional-Change_final.pdf(Öffnet neues Fenster)

I3-MediaRoad and Vital media- EU funded project (Horizon2020)/ I3’s, MediaRoad’s and Vital Media’s Policy Recommendations for the EU’s Next Multi Financial Framework (publication due in October 2018)

Innovation & Cultural Heritage Conference 20 March 2018, Brussels,

Videos, URL: http://www.videliostreaming.com/Paris1/ec.europa.eu/2018-03-20_9h/(Öffnet neues Fenster)

Conference Report: https://ec.europa.eu/info/publications/innovation-cultural-heritage-conference-report_de(Öffnet neues Fenster)

KEA Study: Research for CULT Committee – Creative Europe: Towards the next programme generation, June 2018, URL: http://www.europarl.europa.eu/RegData/etudes/STUD/2018/617479/IPOL_STU(2018)617479_EN.pdf(Öffnet neues Fenster)

Mapping the creative value chains. A study on the economy of culture in the digital age : final report – Study: https://publications.europa.eu/en/publication-detail/-/publication/4737f41d-45ac-11e7-aea8-01aa75ed71a1/language-en(Öffnet neues Fenster)

Morganti L., Ranaivoson H., Mazzoli E.M. (2018), MediaRoad Vision Paper: The Future of Media Innovation. European Research Agenda Beyond 2020, available at:

http://www.mediaroad.eu/vision-documents(Öffnet neues Fenster)

OECD Innovation Strategy 2015, URL: http://www.oecd.org/sti/OECD-Innovation-Strategy-2015-CMIN2015-7.pdf(Öffnet neues Fenster)

Overview of EU policies and studies related to entrepreneurship and innovation in cultural and creative sectors prepared by the EU Commission, DG EAC, for the OMC Group, January 2018, website URL https://publications.europa.eu/en/publication-detail/-/publication/1c3f87fa-2e5a-11e8-b5fe-01aa75ed71a1/language-en(Öffnet neues Fenster)

Promoting access to cultural heritage via digital means, Policies and strategies for audience development : work plan for culture 2015-2018 – Study commissioned by DG EAC, 2017, URL: https://publications.europa.eu/en/publication-detail/-/publication/7839cb98-651d-11e7-b2f2-01aa75ed71a1(Öffnet neues Fenster)

Technology and Innovation for Smart Publishing (TISP) Policy Recommendations, 2014, published in: Smartbook, website URL http://www.smartbook-tisp.eu/recommendations/policy-recommendations-final-edition(Öffnet neues Fenster)

The role of public policies in developing entrepreneurial and innovation potential of the cultural and creative sectors, Report of THE OMC (Open Method of Coordination) working group of Member States’ experts – Study, Apri 2018, website URL

Towards more efficient financial ecosystems. Innovative instruments to facilitate access to finance for the cultural and creative sectors (CCS) : good practice report – Study, DG EAC, 2016, website URL:

UK Report: Culture is digital, UK Dept for Digital, Culture, Media & Sport, 2018

UNESCO Global Report: Re/Shaping Cultural Policies, 2018

VitalMedia – EU funded project (Horizon2020)/ New European Media (NEM): Policy Recommendations on future research and innovation activities in the area of Content, Media, and Creative industries, https://nem-initiative.org/vital-media-project/(Öffnet neues Fenster)

[1] For example, research findings available at the start-up website angel.co shows that, globally, the creative sectors (combining arts, media, entertainment etc.) easily out-perform other sectors such as health when it comes to the number of start-ups. https://angel.co/markets(Öffnet neues Fenster)

[2] “Facebook and Google dominate online ads. Can alliances between news publishers compete?”, by James Rose, Poynter, 24 May 2018, URL: https://www.poynter.org/news/facebook-and-google-dominate-online-ads-ca…(Öffnet neues Fenster)

[3] “Mapping the Creative Value Chains”, study commissioned by the EU Commission (DG EAC), 2017, p. 304, https://publications.europa.eu/en/publication-detail/-/publication/4737…(Öffnet neues Fenster)

[4] http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT+REPORT…(Öffnet neues Fenster)

[5] European Parliament Report: “On a coherent EU Policy for the CCI”, 2016, http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT+REPORT…(Öffnet neues Fenster)

[6] “Mapping the Creative Value Chains. A study on the economy of culture in the digital age”, KEA/IDEA/SMIT, commissioned by the European Commission/ DG EAC, 2017, p. 305, http://www.keanet.eu/wp-content/uploads/Final-report-Creative-Value-Chains.pdf(Öffnet neues Fenster)

[7] 1% for Culture Campaign, Culture Action Europe, https://cultureactioneurope.org/projects/1-percent-for-culture-campaign/(Öffnet neues Fenster)

[8] cf. “Boosting the competitiveness of the creative and cultural sectors for growth and jobs”, page 1, European Commission study EASME/COSME/2015/003, URL: https://ec.europa.eu/growth/content/boosting-competitiveness-cultural-and-creative-industries-growth-and-jobs-0_en(Öffnet neues Fenster)

[9] For example, in the book sector some big players do not use standard formats (like the EPUB) or even well-established standard identifiers like the ISBN for e-books, which inhibits interoperability.

[10] Commission staff working paper, Impact assessment accompanying the Creative Europe Regulation, 2011:

https://bit.ly/2IYtb1Z(Öffnet neues Fenster); the European Commission introduced a “Cultural and Creative Sectors Guarantee Facility” within the Creative Europe programme in 2016 – a step in the right direction, cf. http://www.eif.org/what_we_do/guarantees/cultural_creative_sectors_guar…(Öffnet neues Fenster)

[11] e.g. the NEMO Working Group on Creative Industries and Museums states that “by far the major obstacle to innovation in cultural heritage sector is low awareness among cultural institution managers about challenges and necessities of the digital age”, internal note, Raivis Simansons, NEMO, Creative Museum Thinktank (Latvia).

[12] „Creating Growth. Measuring cultural and creative markets in the EU“, study by Ernst & Young, 2014, p. 25

[13] ibd.

[14] Eurostat, EU Government expenditure by function, 2017, http://ec.europa.eu/eurostat/statistics-explained/index.php/Government_…(Öffnet neues Fenster)

[15] a recent study states that “Overall, there is much more data available for the European audiovisual market than there is for the cultural sectors, due mainly to the work of European Audiovisual Observatory, a high capacity research body:” cf.: KEA Study: Research for CULT Committee – Creative Europe: Towards the next programme generation. URL: http://www.europarl.europa.eu/RegData/etudes/STUD/2018/617479/IPOL_STU(2018)617479_EN.pdf(Öffnet neues Fenster), p. 29, cf also: KEA Feasibility study on data collection and analysis in the cultural and creative sectors in the EU. A study prepared for the European Commission, DG EAC. Brussels, 2015. The Copyright Hub (http://www.copyrighthub.org(Öffnet neues Fenster)) is particularly interesting because of its cross-sectoral nature. Initially an initiative supported by the UK government, it was able to scale up at international level. However, it lacks public-sector support. The EDRLab (https://www.edrlab.org(Öffnet neues Fenster)) stems from the international cooperation in the e-book sector. It receives public support from the French Government only.

[17] cf. press release: EU budget: New Single Market programme to empower and protect Europeans, 7 June 2018, URL: http://europa.eu/rapid/press-release_IP-18-4043_en.htm(Öffnet neues Fenster)

[18] cf. press release: EU budget: Commission proposes EUR 9.2 billion investment in first ever digital programme, 6 June 2018, URL: http://europa.eu/rapid/press-release_IP-18-4049_en.htm(Öffnet neues Fenster)

[19] cf. https://ec.europa.eu/commission/sites/beta-political/files/budget-june2…(Öffnet neues Fenster)

[20] press release: EU budget: Reinforcing Europe’s cultural and creative sectors, 30 May 2018, http://europa.eu/rapid/press-release_IP-18-3950_en.htm(Öffnet neues Fenster); a recent study states the high demand – and the low success rate of 16% in the cultural sub-sector of Creative Europe, KEA: Towards the next programme generation, p. 59

[21] overall planned EU budget 2021-2027; EUR 1,135 billion, cf. http://europa.eu/rapid/press-release_IP-18-3570_en.htm(Öffnet neues Fenster)

[22] Press release: EU budget: Stepping up the EU’s role as a security and defence provider, 13 June 2018, URL: http://europa.eu/rapid/press-release_IP-18-4121_en.htm(Öffnet neues Fenster)

[23] cf cf. https://ec.europa.eu/commission/sites/beta-political/files/budget-june2…(Öffnet neues Fenster)

[24] cf. Cultural and Creative Sector Guarantee Facility, URL: https://ec.europa.eu/programmes/creative-europe/cross-sector/guarantee-…(Öffnet neues Fenster)

[25] the annual ARD/ZDF Academy is a good example for initiatives like this, as are the Media Labs in journalism, which support the development not only of products but also of people, skills and mindsets. cf. the Global Alliance for Media Innovation (GAMI) http://media-innovation.news/(Öffnet neues Fenster)

[26] KEA European Affairs, website URL http://slideplayer.com/slide/6913301/23/images/4/CREATIVE+INDUSTRIES+AND+ACTIVITIES+User+Generated+Content.jpg(Öffnet neues Fenster)